The declarations page is an important part of your home insurance policy that provides vital information. It summarizes your coverages and limits, lists your premium and deductible and also provides contact and policy information.

Written by Chris Kissell

Chris Kissell

Chris Kissell is a Denver-based writer and editor with work featured on U.S. News & World Report, MSN Money, Fox Business, Forbes, Yahoo Finance, Money Talks News and more.

Reviewed by Leslie Kasperowicz

Leslie Kasperowicz

Leslie Kasperowicz is an insurance educator and content creation professional with nearly two decades of experience first directly in the insurance industry at Farmers Insurance and then as a writer, researcher, and educator for insurance shoppers writing for sites like ExpertInsuranceReviews.com and InsuranceHotline.com and managing content, now at Insurance.com.

Updated on : April 15, 2024Why you can trust Insure.com

At Insure.com, we are committed to providing the timely, accurate and expert information consumers need to make smart insurance decisions. All our content is written and reviewed by industry professionals and insurance experts. Our team carefully vets our rate data to ensure we only provide reliable and up-to-date insurance pricing. We follow the highest editorial standards. Our content is based solely on objective research and data gathering. We maintain strict editorial independence to ensure unbiased coverage of the insurance industry.

A homeowners insurance policy protects your home, valuables and even your life savings when something goes wrong. The homeowners insurance declaration page provides all of the key details of your policy in one place.

The declarations page is usually the front page of your home insurance policy and tells you what coverages you have purchased, how much the coverage costs and your coverage limits. It also lists the insurance company, agent if you have one and your deductible.

It’s important to know how to read the declarations page in order to understand your coverage. Fortunately, it’s not complicated.

Key Takeaways

Understanding the basics about your declarations page – and where to find it – will make it easier to find the information you need about your policy. Although the page may differ slightly from company to company and policy to policy, a declaration page’s basic structure is similar across the industry.

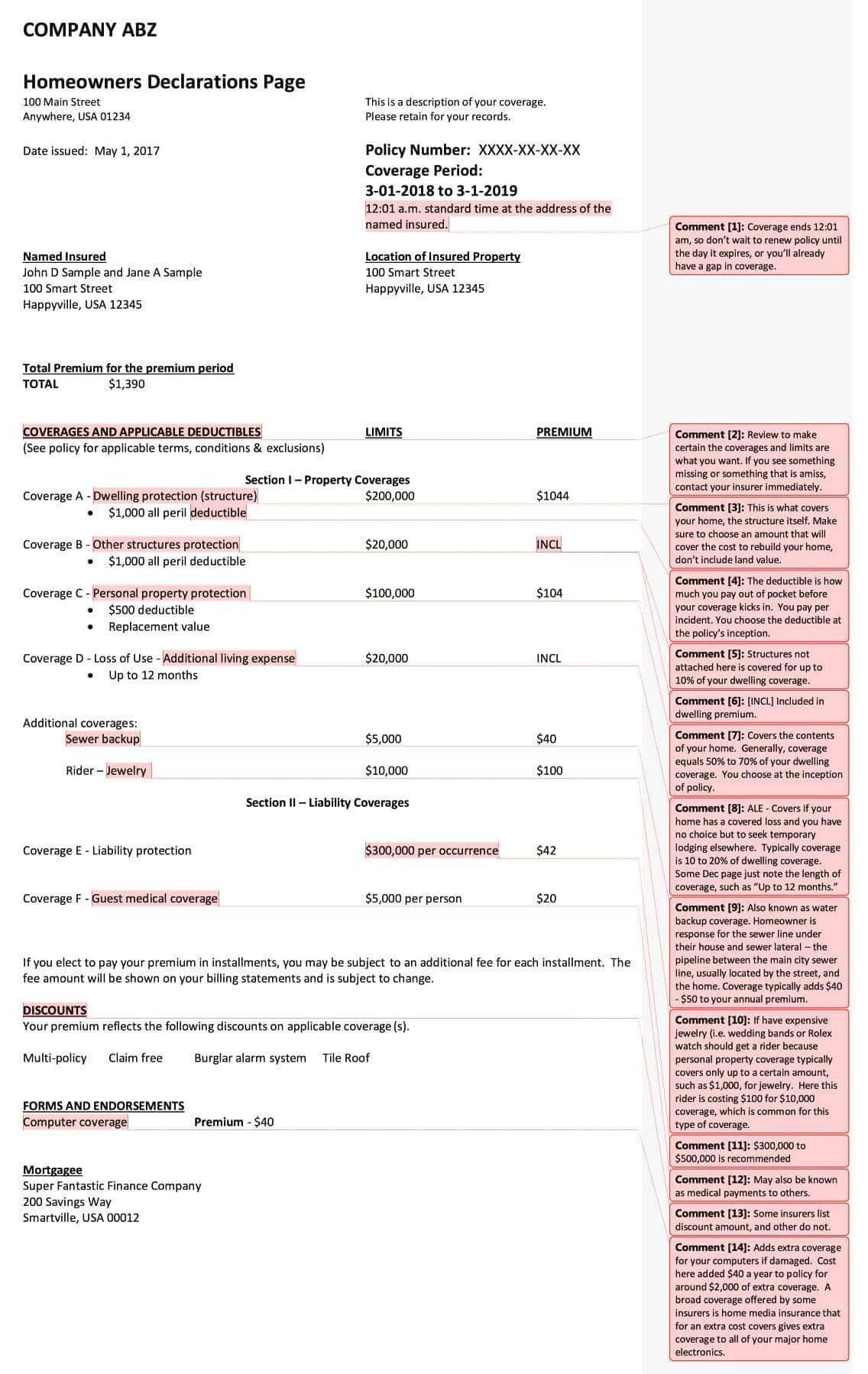

Here’s a look at a sample declarations page.

A homeowners declaration page summarizes your coverages, as well as your personal and home information.

The page lists all parties involved with the policy in any way. This includes you — as the named insured party — your insurance agent or company and your mortgage company.

On the declaration page, you will find basics such as:

However, the most important part of the homeowners insurance declaration page is the coverage types and limits that apply to your policy. The declarations page lists how much coverage you have for:

You may also see any endorsements, like extended replacement cost, that you have added listed here.

The declaration page also lists the premium amount you are paying for the coverage, the deductible that applies to the policy and any discounts applied to your policy.

It is important to note that the declarations page is designed to be a readable summary for the homeowner. It is not intended to list every coverage you have down to the smallest detail. For that information, you will have to dig deeper into the policy or contact your agent.

A new homeowners insurance declaration page will be sent to you at the beginning of each new policy period. The declaration page is usually one of the first pages in the policy documents that your homeowners insurance company sends you at renewal.

It is important to keep this page for your records. In addition, your mortgage lending company may require you to send a copy of the declarations page. In most cases, the insurance company will send a copy directly.

Typically, the top of your declaration page will include your name and the insured property’s address. You will also see your premium amount prominently displayed.

Your policy number and the policy period are among the most important features you will see on the top half of the page.

Pay close attention to the policy period. The declaration page will likely include a notation that the policy period ends at “12:01 a.m. standard time at the address of the named insured.” It is crucial to renew your policy before the time and date listed. Otherwise, you could have a gap in your coverage.

As you move down the page, you will see a list of your coverages, the limits of those coverages, and how much each portion of coverage costs. For example, you may see a listing for “Coverage A — Dwelling premium” that includes the limits of the coverage, your deductible for that coverage and how much you pay in premiums for the coverage.

Below the coverages, you will see the discounts that have been applied to your policy. If you don’t see any discounts — or you are interested in learning if you qualify for more — contact your insurance agent.

Finally, you will see any endorsements to your policy that you may have purchased – for example, extra coverage for expensive computer equipment.

Give the declaration page a thorough reading. Review the personal information for errors, and check that it reflects the proper coverage levels, as well as any additional riders you may have added.

Insurance companies are required to write policies in a language that the insured can understand. However, insurance does have its own terminology, and it’s important to learn some of it. Here are just a few definitions you should be aware of when reading your policy:

This type of coverage reimburses you for the full cost of replacing a destroyed or stolen item, regardless of how much the item has depreciated in value. Because replacement cost coverage is more robust than actual cash value coverage, it tends to be more expensive.

This type of coverage considers an item’s depreciation when calculating your payout. So, if your stolen or destroyed TV was 15 years old, you will get a check for the depreciated cost, not a check for what a similar brand-new TV would cost today. This type of coverage is less expensive than replacement cost coverage.

Endorsements are extra coverages that you can choose to add for additional coverage. They can provide coverage for an otherwise excluded peril, or increase coverage levels.

Add-ons, such as coverage for identity theft or a recent storm, can help you get more out of your policy. Home daycare coverage is just one of the many endorsements available. It may be a good idea to add scheduled endorsements for high-value items such as antiques or jewelry, which increase the limits of coverage and can make the payout greater in case of loss.

This is the amount you must pay before your coverage kicks in. Typical deductible amounts are $500 to $1,000. In addition, you may have separate deductibles for things like wind or hail damage.

You will see all of the main coverages that are part of your home policy on the

This applies to the structure of the home itself. On a standard home insurance policy, this is the replacement cost of your home. That’s the amount required to rebuild it from the ground up.

This covers structures that are not attached to the house. This might include things like detached garages, fences, sheds, in-ground swimming pools and gazebos. This is usually set at 10% of the dwelling coverage.

This applies to personal items such as furniture, appliances, clothes and other possessions; all of the contents of your house are covered. Typically, your coverage amount for personal belongings is 50% to 70% of your dwelling coverage, but there are special limits on some types of property.

This coverage, also called loss of use coverage, reimburses you for living expenses if you are unable to live at home due to damage from a covered loss.

Any additional coverages included with your policy will be listed here, such as endorsements.

This protects you in the event of a lawsuit when you or a family member are responsible for bodily injury or property damage to someone else. It also covers damages caused by your pets, such as a dog bite. You are covered for both the cost of hiring a lawyer and for any damages you might owe.

This provides no-fault guest medical coverage to pay the medical bills if someone is injured in your home.

An HO-3 policy is an all-perils or open-perils policy. This means that all perils are covered unless they are specifically excluded. In general, an HO-3 policy excludes coverage for loss or damage resulting from these perils:

Homeowners insurance offers crucial protections for what is likely to be your most significant investment. However, to get the most from this coverage, you need to understand what your policy does and does not cover to determine if you have the right coverage and enough of it.

Here are a few tips from industry experts to help you navigate the world of homeowners insurance.

Review your quote with an expert. Homeowners insurance can be tricky, so it pays to consult an expert after narrowing down your choices from a batch of quotes.

“Never shop on price alone, as you usually get what you pay for,” says Kristofer Kirchen, president of Advanced Insurance Managers.

Also, remember that if you bundle your coverage with one insurance company, you may net additional savings.

Coverage levels are key. Understanding your coverage levels is important.

“There is nothing worse than receiving a bill for an insurance-related fix and having the insurance company not cover all of it due to a technicality in the policy,” says Sacha Ferrandi, founder of Source Capital Funding.

Read your declaration page and policy carefully. Understanding exactly what is covered and how your policy works is important. Overlooking minor details can have major consequences.

“Many states have instituted separate deductibles for wind and hail, and many policyholders don’t understand them,” says Travis Biggert, President (Oklahoma and Arkansas), Hub International.

Add-ons can be worth it. There are a number of riders that can be added to a policy, and many of them are well worth the price.

“Consider adding sewer and drain backup coverage to your homeowners policy. It is one of the most common homeowners claims, averaging $10,000-$20,000 in expenses, and it is almost always excluded from a basic policy,” says Bret Boizelle, vice president with Boizelle Insurance Partnership.

Shop smart: The cost of homeowners insurance has been on the rise for a number of years, so shopping for your coverage regularly has never been more important.

“It’s very important to be a smart consumer and shop your policy on a regular basis,” says Carole Walker, executive director of the Rocky Mountain Insurance Information Association.